Monthly Review December 2022

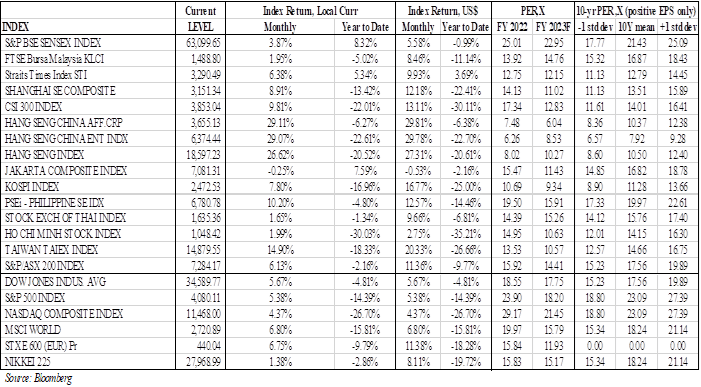

The best performing regional indices were H-shares (+29.07% in local currency term), Hong Kong (+26.62%) and Taiwan (+14.90%), while the laggards were Indonesia (-0.25%) and Vietnam (-1,99%). Malaysia and Thailand chalked up a small gain of 1.95% and 1.65% respectively in local currency term, but strong appreciation of the Ringgit and Thai Baht against the USD boosted KLCI and SET to gain 8.46% and 9.66% respectively in USD term. Regional currencies were mostly strong against the USD. The best performing currencies were Thai baht (+8.35 %) and Korean Won (+8.08 %), while the worst were Indonesia Rupiah (-0.85%) and Vietnamese Dong (+0.55%).

The best performing regional indices were H-shares (+29.07% in local currency term), Hong Kong (+26.62%) and Taiwan (+14.90%), while the laggards were Indonesia (-0.25%) and Vietnam (-1,99%). Malaysia and Thailand chalked up a small gain of 1.95% and 1.65% respectively in local currency term, but strong appreciation of the Ringgit and Thai Baht against the USD boosted KLCI and SET to gain 8.46% and 9.66% respectively in USD term. Regional currencies were mostly strong against the USD. The best performing currencies were Thai baht (+8.35 %) and Korean Won (+8.08 %), while the worst were Indonesia Rupiah (-0.85%) and Vietnamese Dong (+0.55%).

For the month of November 2022, the MSCI Far East ex-Japan Index gained 21.91%, compared to the MSCI World Index’s 6.80% gain. The huge outperformance of the Far East ex-Japan markets was driven by sharp gains in Chinese risk assets. The ASEAN Index underperformed within the Asia region.

Risk assets performed positively in November. Major indices in the US gained on announcement of better-than-expected inflation data which led to expectation that it may prompt the Fed to slow down rate increase. Dow Jones Industrial Average (DJIA), S&P 500 and Nasdaq Composite returned 5.67%, 5.38% and 4.37% respectively. The US October headline CPI came in at 7.7% YoY, easing from the previous month. Core prices, which exclude food and energy, reduced from a 40-year high and came to 6.3%. US 10-year yields fell from 4.05% to 3.61%, with the two-year dropping from 4.49% to 4.34%. Industrial activity slowed in November, with the flash composite purchasing manager’s index (PMI) – an indicator of business activity – retracting to 46.4 from 48.2 in October. A figure below 50 indicates slowing activity.

The Stoxx Europe 600 Index gained 6.75%. European Central Bank (ECB) raised its key interest rates by 75 basis points. Shares were supported by hopes that inflation may be moderating in the eurozone. Eurozone inflation, as measured by the consumer price index, eased to 10.0% YoY in November, from 10.6% in October. Warmer autumn weather resulted in reduced energy demand, although energy costs remain the biggest component driving higher inflation.

Hong Kong and H shares indices gained sharply, with Hang Seng Index and Hang Seng China Enterprises Index gaining 26.62% and 29.07% respectively. China’s A shares index also gained 13.11%. China’s expansionary monetary policies improved market sentiments, driving risk assets higher. In a meeting held to study measures to stabilize the economy, the State Council, chaired by Premier Li Keqiang, called for using more monetary policy tools, including cutting RRR “in a timely and appropriate manner” to better support the real economy. It also encouraged banks to offer loans to ensure a “healthy development” of property market, and called for better supports for private firms’ bond sales

South Korea’s KOSPI Index gained 7.80% on bargain hunting. Bank of Korea (BOK) raised interest rate by 25bps to 3.25% while also cutting its 2023 growth outlook to 1.7% from 2.1% but keeping its 2022 projection intact at 2.6%. BOK Governor Rhee signaled the rate hike cycle may be coming to an end, and suggested a terminal rate of roughly 3.5%. Three board members saw one more hike on the horizon, while one member thought that the rates had been raised enough.

Taiwan’s TWSE Index gained 14.90% on improved investors’ risk appetite. However, Taiwan’s consumer confidence weakened in November to the lowest level in nearly thirteen years. The consumer confidence index dropped to 60.0 in November from 61.2 in the previous month

Singapore’s STI gained 6.38%. Singapore’s manufacturing production declined by 0.8% YoY in October, compared with market consensus of a 0.9% drop and after a downwardly revised 1.6% gain in September. This was the first fall in factory output since September 2021, due to a slump in biomedical manufacturing (-14.5% vs -1.4% in September), led by pharmaceuticals (-27.1%). On a monthly basis, manufacturing output rose by 0.9% in October, the third straight month of gain, defying expectations of a 0.3% fall.

Malaysia’s KLCI gained 1.95%. Inflation slowed to 4.0% YoY in October from 4.5% in

September. Core inflation rose by 0.1 percentage point to 4.1% YoY, putting it above the headline reading. While the general election did not result in any coalition party winning a majority of the seats, the subsequent formation of a Pakatan Harapan-led coalition with the Umno-led Barisan National and Sarawak’s GPS and the appointment of Anwar Ibrahim as Prime Minister is viewed positively by the market.

Thailand’s SET Index gained 1.65%. Thailand’s headline CPI eased to +6% in October as energy costs slowed while food prices finally showed signs of peaking despite concerns on the impact of floods. Core inflation inched up slightly to +3.2%. Upside pressures remain from the weaker Baht, flooding impact on food prices, and the increase in minimum wages on 1 October.

Jakarta Composite Index declined 0.25%. The Organization for Economic Co-operation and Development (OECD) cut Indonesia’s growth projection for 2023 to 4.7%, down from the previous prediction of 4.8%. The decrease was made because of the threat of a global recession next year.

The Philippines PSE Index rallied 10.20% after the sharp correction in the previous month. Philippine Central Bank (BSP) raised its policy rate by another +75bps to 5.00%, the sixth successive hike giving a total +300bps hike so far this year. BSP raised its inflation forecast for 2022 and 2023 to +5.8% (vs. +5.6% previously) and +4.3% (vs. +4.1% previously), respectively. The inflation rate is expected to stay above BSP’s target range of 2%-4% until mid-2023.

Vietnam’s VN-Index gained 2.75% on bargain hunting. Vietnam posted a trade surplus of US$9.4 billion in the first ten months of 2022, compared to US$630 million in the same period last year, according to the General Statistics Office (GSO). In October, the country’s total export and import value was estimated at US$58.27 billion, up 0.1% MoM and 5.7% YoY.

The contraction in economic activities and slower economic growth outlook continued to worry global investors. The potential demand disruption from slower growth has started to be manifested in weaker corporate earnings guidiance. The Federal Reserve’s pronouncements of its stance on rates hikes has continued to affect investors’ sentiment and bring about trading volatility. The lower October headline CPI at 7.7% YoY, easing from the previous month improved investors’ expectation on a slow down of the pace of interest rate increase.

The corrections in recent periods present opportunity, especially in Asia ex. Japan, in particular Chinese equities on depressed valuation. The positive impacts of expansionary Chinese policies to support economic activities and indications of changes in Covid control management policies has resulted in market interpretation as prelude to the relaxation of the zero-Covid strategy. This is viewed positively by the market.

We are watchful of developments in the Russia-Ukraine conflict as well as policy directions in the major economies, in particular US and China, which will have major implications on economies in general as well as on specific sectors. US policy responses will continue to face headwinds going into 2022. Tapering and rate hikes in 2022 will affect liquidity and increase cost of borrowing in the system, not just in the US but world wide. In Asia, the focus is on China’s policy measures to spur economic activities and revive growth in the property sector, and the developments in China’s responses to Covid-19 situation there.

While we are more cautiously optimistic, there remains headwind for risk assets, including rising bond yields and interest rate hikes, and the relatively high commodity prices (although these have come off to some extent), as well as the still relatively high valuations in the developed markets. The heightened geo-political issues between China and US, and the tension between US/Europe and Russia over Ukraine will keep risk premium elevated at times and result in markets volatility.

We continue to apply our strategy of focusing on identifying fundamentally healthy companies with low valuations, low leverage, high growth, robust management and a strong track record, and adherence to our investment philosophy of “Never Fully Invest at All Times” which has served us well over the years. We are also in the midst of developing a robust ESG investment framework to meet the increasingly socially-aware demands of investors, as well as other stakeholders.

We thank you once again for your continued faith in us, and hope to remain good stewards in our endeavour to protect and grow your capital.

This advertisement is solely for information purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, investment product or service. The information contained herein does not have any regard to the specific investment objectives, financial situation or particular needs of any person. Investors may wish to seek advice from a financial advisor before making any investment decision. Past performance is not indicative of future results. An investment is subject to investment risks, including the possible loss of the principal amount invested.