Welcome To

Pheim

Unit Trusts Berhad

Pheim Unit Trusts Berhad (PUTB) started its operation in April 2001. We are a Unit Trust Management Company approved by the Securities Commission, and a wholly-owned subsidiary company of Pheim Asset Management Sdn Bhd (PAMSB)

Read More

Market Review

Risk assets started the year on a positive note, heading higher with volatility amid geopolitical tensions. The World Index gained 2.19% in January. The MSCI Far East Ex. Japan index outperformed, gaining 10.96%, driven by North Asia markets, in particular Korea and Taiwan markets. Within the Asia region, ASEAN equities gained +4.82%, led by Singapore (+5.57%) and Malaysia (+3.62%) markets. The performance of regional currencies was mixed against the USD. The best performing currencies were Malaysia Ringgit (+2.88%) and Vietnamese Dong (+1.35%), while the weaker ones were Indonesia Rupiah (-0.63%) and Hong Kong Dollar (-0.40%).

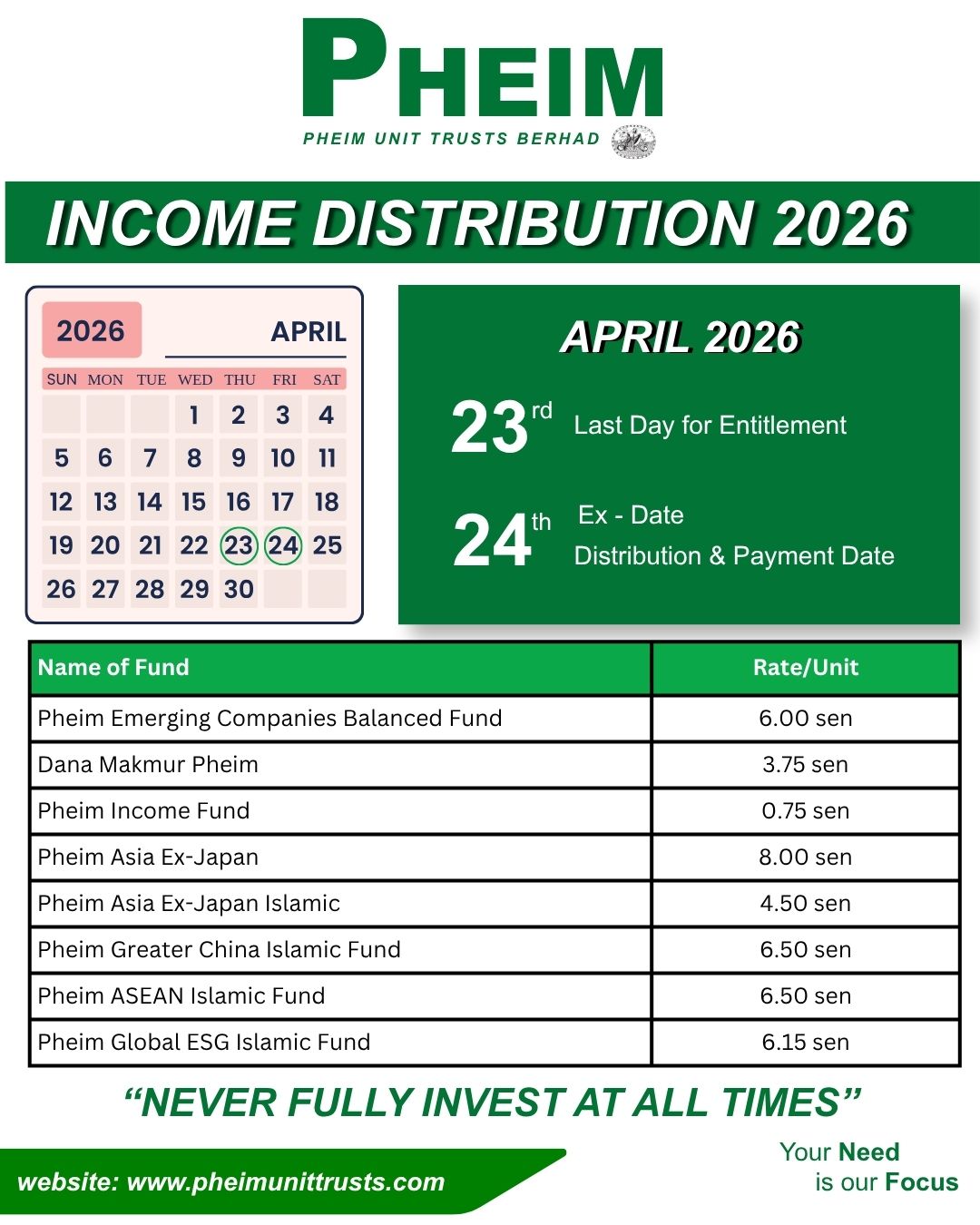

Funds Income Distribution

Please be informed that the following funds are paying income distribution for 2026