Market Review April 2026

Market Outlook Ex-Japan

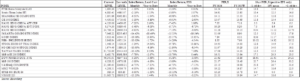

Risk assets corrected sharply amid escalating Middle East war when the US and Israel launched unilateral pre-emptive strikes on Iran on February 28. In retaliation, Iran closed the Strait of Hormuz through which about 20% of crude oil and LNG exports from the Gulf pass through, resulting in higher energy prices across the globe. Treasury yields moved materially higher. Key stable macro variables face challenging headwind as market expectation on inflation rate is likely to move higher. The magnitude and severity of the impact on inflation and the world economic growth will rest upon the duration of the US/Israel and Iran war. The World Index declined 6.55% in March. The MSCI Far East Ex. Japan index underperformed, declining 13.69%, driven by North Asia markets, in particular Korea and Taiwan markets which are more dependent on energy imports from the Middle East. Within the Asia region, ASEAN equities declined 7.38%, led by Indonesia (-14.42%) and Vietnam (-10.95%) markets. Regional currencies weakened against the USD. The best performing currencies were Hong Kong dollar (-0.20%) and Chinese Yuan (-0.47%), while the weaker ones were Philippines Peso (-5.07%) and Korean Won (-5.03%).

US indices corrected across the board on risk aversion due to heightened geopolitical tension in the Middle East. For the month, Dow Jones Industrial Average (DJIA), S&P 500 Index and Nasdaq Composite declined 5.38%, 5.09% and 4.75% respectively. The US economy slowed as the first revision of the 4Q GDP reading was lower than the previous quarter estimate and well below the Dow Jones consensus forecast of 1.5% growth rate. It is also a considerable slowdown from the 4.4% gain in the prior period, hampered by a record long government shutdown that saw the government spending tumbled 16.7%. Although the US is a net exporter of crude oil, it is nevertheless facing substantial price increases in gasoline and oil products due to global price shocks and supply chain disruptions. Given the prevailing market situation, the Fed is expected to be reluctant to shift any time soon. The IMF sees little room for the Fed to cut interest rates in 2026.

The Stoxx Europe 600 Index corrected 8.00% from the prior month as energy price surged and inflation climbed to 2.5% in March from 1.9% in February, exceeding the European Central Bank (ECB)’s 2% target. The ECB held the interest rate at 2% in March, maintaining a cautious stance on elevated inflation risks. The unemployment rate in the Euro Area edged up to 6.20% in February 2026, rising from 6.10% in January. The energy and defensive sectors performed relatively better.

Hong Kong and H shares indices continued to soften. Hang Seng Index and Hang Seng China Enterprises Index declined 6.92% and 5.48% respectively as concerns over slower China economic growth and geopolitical risks weighed on investors’ risk appetite. During China’s Two Sessions meeting in March, the Government Work Report sets key economic and social goals, lowering the growth target from 5% in 2025 to 4.5%-5% in 2026. The adjustment aims to allow 2026 economic policies to focus more on improving growth quality while creating room for structural adjustments, reforms, and risk prevention.

South Korea’s KOSPI Index corrected sharply, declining 19.08% in March driven by negative news flow in memory sector and geo-political development in the Middle East, as well as profit taking after the sharp 48.28% run in the first two months of the year. There were concerns over future memory demand due to Google’s newly introduced TurboQuant technology that can reduce memory usage per task by up to six times. Economic activities remained robust. Korea’s industrial output posted its fastest growth in five years and eight months in February, mainly driven by gains in semiconductor production. The semiconductor production surged 28.2% from a month earlier, on the back of growing global demand driven by the artificial intelligence (AI) boom.

Taiwan’s TWSE Index declined, dropping 10.42% on profit taking. The market had risen 22.98% in the first two months of the year. Economic indicators remained healthy. Taiwan’s economic monitoring indicator flashed a red light for the third straight month in February, with the composite score rising to its highest level in more than four years according to the National Development Council (NDC). The composite index climbed one point from a month earlier to 40, the highest since July 2021, remaining in the red zone that signals an overheating economy.

Singapore’s STI corrected by 2.19% in March on global risk-off sentiment. Economic activities remained resilient. The S&P Global Singapore PMI jumped to 59.2 in February 2026 from 56.8 in January, marking the thirteenth consecutive month of expansion and the second-fastest pace on record. New orders rose at the quickest rate in 18 months, supported by stronger domestic and external demand, while output expanded historically fast, led by transport, information and communication.

Malaysia’s KLCI declined 1.53% on profit taking. Bank Negara Malaysia, somewhat surprisingly, expects economic growth of between 4%-5% this year, revising its forecast slightly upwards from 4%-4.5%, supported by strong household spending. Inflation was expected to remain moderate in 2026, in part due to policies aimed at cushioning the impact of rising commodity and energy prices

Thailand’s SET Index declined 5.24% in March on profit taking after registering strong gain year to date. Thailand’s consumer confidence index rose to 53.7 in February 2026 from 52.8 in January, marking the highest level since last May. The improvement was supported by the central bank’s rate cut to 1% and expectations that the new government after last month’s elections would introduce economic measures, including policies to provide cushion from high energy prices, promote household consumption, boost tourism and promote trade and investment incentives and farming support.

Jakarta Composite Index declined 14.42% on continued outflow by foreign investors. Indonesia retail sales accelerated to 6.9% YoY in February (from 5.7% in January), driven by food & beverages and household equipment spending, with the Ramadan season lifting monthly growth to +4.4% MoM. However, Consumer Confident Index softened to 125.2 (from 127 in January), reflecting weaker sentiment among lower- and upper-income households on income and job prospects, while middle-income confidence edged up on improved job outlook.

The Philippines PSE Index declined 10.02%. The S&P Global Philippines Manufacturing PMI rose to 54.6 in February 2026 from 52.9 in January, reflecting stronger manufacturing activity supported by sustained growth in new orders and the fastest pace of output expansion since November 2018. Inflation edged higher to 2.4% YoY in February 2026 from 2.0% in January, in line with market expectations and remaining within the central bank’s target range.

Vietnam’s VN-Index declined 10.95%. Foreign investors were net sellers throughout the month. Domestically, tightening systemic liquidity is a growing concern; with several commercial banks now pushing 12-month deposit rates above 9%.

MARKET OUTLOOK

The shift to a dovish monetary stance in the US at the start of 2026 appears now to have been upended by the war in the Middle East. After an almost 12 months of twist and turns in the US tariff saga, the market is still divided on impact of higher tariffs on macro variables such as inflation and economic activities. Meanwhile, US corporate earnings, especially in the technology sector, continue to be key pillar to hold up risk assets. US market valuations are at historical high, and the high valuation is further driven by strong capital expenditure drive for AI, which has raised questions as to whether the humongous expenditures in AI will generate the anticipated returns. The semiconductor and AI investment cycle may move into a more difficult phase as investors will start to be more discerning with regard to their return on investment. The supply and demand dynamic in the semiconductor cycle, on the margin, with supply capacity gradually improving at a time when global demand soften on lower GDP growth outlook, can potentially result in headwinds for the industry.

Geo-political developments as well as policy directions in the major economies, in particular US and in China, remain on our radar screen. The market is still watchful of developments in Trump’s tariffs for the key trade partners. Following the US Supreme Court’s recent ruling that the Trump Administration’s reciprocal tariffs are illegal, and the subsequent announcement by Trump to impose a new 15% tariffs on imports, uncertainties remained. The market is also attentive to other US policy pronouncements that would have major fiscal, financial and economic implications. Investors, by and large, appear to be comfortable with Trump’s “Big Beautiful Bill” that has been signed into law, notwithstanding that it will substantially increase US federal deficit and government debt. Meanwhile, new geo-political fissures have opened up with the recent US military raid and capture of Venezuela President, Nicolas Maduro Moros, and the repeated utterings by President Trump of his intention to bring Greenland within the US fold, militarily if necessary. Adding to these is the flare up of the military conflict between the US/Israel and Iran that has engulfed the entire Middle East and choked the supply of crude oil and LNG from the region to the world. These developments further heightened tension in global geo-politics. In the near term, the US mid term election to be held in the later part of 2026 may change the balance of power in the US Congress, and have significant impact on US policies in the remaining years of Trump’s term. These developments will create uncertainities for investors. The duration of the Middle East war has added to uncertainty in global growth outlook as supply chain disruptions in energy sources among other things push inflation higher and change macro variables assumption.

In Asia, the focus is on the pace of China’s economic recovery which has been weaker than expected. The tariff issues with the US and continuing efforts to broaden restrictions on sales of tech equipment and services to Chinese entities can only exacerbate the economic situation in China. The Chinese property sector continues to face challenges, and any sign of stabilization and growth will have positive catalyst for China’s economy and risk assets. The Chinese government continues to bring forth measures to help the economy. The Chinese government remains constructive on policies to spur economic activities to achieve economic growth target. The various measures have boosted market sentiments. However, the longer- term effectiveness on China’s economy continues to be closely watched. It may take time for the initiatives to bear fruits. The focus will be on addressing the challenges in the property market, lifting consumer sentiments and consumption, and countering the effects of the new US tariffs.

On external trade, countries with high export dependency for growth in the Asia region including ASEAN will face significant challenges arising from the US tariff policies. The disruption in supply chain realignment may result in temporary mismatch in corporate earnings delivery against market expectation during the initial stage of tariff implementation. To-date, while ASEAN countries’ exports to the US have been impacted by the tariffs, these countries have been able to mitigate the impact on the economic growth through trade diversifications. Many of these countries have now to also contend with having to manage disruptions in energy supplies and the ensuing price escalations.

While interest rates have started to be eased, there remains headwind for risk assets, including the impact of the still high interest rate on business and economic activities, uncertainties in US policies, the historically high market valuations in the US, the geo-political tension in

various parts of the World and resulting disruptions to energy supplies, as well as the still slower than expected economic growth in China. However, in the investment space we are in, we believe there is room for cautious optimism. After years of prolonged sell down, and despite the upticks in recent months, China equities remain under-owned and their favourable valuation offer potential upside, particularly following the recent rounds of significant policy change initiatives from China.

INVESTMENT STRATEGY

We continue to apply our strategy of focusing on identifying fundamentally healthy companies with low valuations, low leverage, high growth, robust management and a strong track record, and adherence to our investment philosophy of “Never Fully Invest at All Times” which has served us well over the years.

We thank you once again for your continued faith in us, and hope to remain good stewards in our endeavour to protect and grow your capital.

MALAYSIA

Market Summary

The FBMKLCI Index decreased 1.53% month-on-month to close at 1,690.36 points. YTD has increased 0.61%. The RM depreciated 3.86% month-on-month against the USD, and closed at MYR 4.05 for the month of March.

Economic News

Malaysia’s financial position strengthened, with international reserves rising to USD128.3 billion as of 27 February 2026, according to Bank Negara Malaysia. This marks the highest reserve level since 2014 and provides a robust buffer against external shocks, including currency volatility and capital outflows.

Malaysia’s headline inflation moderated further in February 2026, easing to 1.4% year-on-year from 1.6% in January, according to the Department of Statistics Malaysia. The slowdown was primarily driven by softer price increases in key components such as insurance, education, and food and beverages, indicating a gradual stabilization in consumer price pressures. On a month-on-month basis, the Consumer Price Index (CPI) rose marginally by 0.2% to 136 points, suggesting that inflation remains contained and broadly in line with stable domestic demand conditions.

Malaysia’s Producer Price Index (PPI) declined by 3.4% year-on-year in February 2026, reflecting easing cost pressures at the upstream level across major sectors, including agriculture, mining, and manufacturing, as reported by the Department of Statistics Malaysia. The contraction in producer prices suggests that input costs have softened, likely due to lower commodity prices and moderating global demand. This trend indicates reduced cost burdens for businesses and may serve as a leading indicator of further moderation in consumer inflation, although the transmission to end prices may be gradual due to lag effects and margin adjustments within supply chains.

In response to escalating global energy prices linked to geopolitical tensions in the Middle East, the government has introduced targeted policy measures to manage fiscal exposure and consumption. Prime Minister Anwar Ibrahim announced a temporary reduction in the subsidised fuel quota under the Budi95 scheme, effective April 1, 2026. The monthly quota for RON95 petrol will be reduced from 300 litres to 200 litres per individual, while the subsidised price remains unchanged at RM1.99 per litre, significantly below the estimated unsubsidised market price of RM3.97 per litre.

This measure reflects a calibrated approach to contain subsidy costs while maintaining price support for consumers. By limiting the volume of subsidised fuel, the government aims to improve fiscal sustainability without fully exposing households to elevated global fuel prices. The policy is explicitly temporary, pending stabilization in global energy markets, although near-term visibility remains limited. At the same time, Malaysia faces emerging external trade risks. The Office of the United States Trade Representative has initiated a Section 301 investigation into Malaysia over concerns of excess manufacturing capacity in sectors such as electronics, machinery, and steel. This development could pose downside risks to Malaysia’s export-oriented industries if it leads to trade restrictions or tariffs. Given Malaysia’s heavy reliance on exports, particularly in electronics especially any escalation in trade tensions could impact industrial output, investment sentiment, and overall economic growth.

Corporate News

Sunway Healthcare Holdings delivered a strong debut on the domestic stock exchange, marking Malaysia’s largest initial public offering in nearly a decade. The company raised approximately RM2.86 billion, and its shares surged by 28% on the first day of trading, reflecting robust investor demand despite broader market volatility. The IPO was supported by prominent institutional investors, including the Malaysian units of AIA, the Employees Provident Fund, and JPMorgan Asset Management, while the retail tranche was oversubscribed by 5.6 times. Operationally, Sunway Healthcare benefits from strong fundamentals in Malaysia’s private healthcare segment, anchored by its flagship facility, Sunway Medical Centre, the largest private hospital in the country. The group typically operates with relatively high EBITDA margins in the range of 20–25%, supported by premium healthcare services and growing medical tourism demand. The key catalyst post-listing lies in its capacity expansion strategy, as IPO proceeds are earmarked for hospital expansion and potential regional growth opportunities. Over the medium term, continued demand for private healthcare and cross-border patients is expected to support earnings growth.

Petronas Chemicals Group Berhad is expected to benefit significantly from the ongoing supply disruptions triggered by the Middle East conflict, with fertiliser and petrochemical prices rising sharply amid constrained global production. Urea prices in Southeast Asia have surged by approximately 47% to around US$720/t, approaching the US$750/t assumption for 2Q–3Q26F, as the closure of the Straits of Hormuz has disrupted about 30% of global urea exports. Further upside risks persist due to prolonged outages in key gas facilities, including 14% of Iran’s South Pars and 17% of Qatar’s gas production, alongside India’s potential 31% cut in domestic urea output, which may increase import demand. As a result, average fertiliser and methanol (F&M) selling prices for PCG are now projected to rise by 40% year-on-year in FY2026 (up from 25% previously). In the olefins and derivatives segment, polyethylene (PE) prices have already increased by about US$450/t since the conflict began, with expectations of a US$500/t uplift sustained over 2Q–3Q26F, supporting a 15% year-on-year price increase assumption. Supply tightness is further reinforced by a projected 10% month-on-month drop in ethylene production in North and Southeast Asia and declining operating rates to 71%. These dynamics underpin a 44% upward revision in FY2026 core net profit with valuation expanded to 1.4x P/BV (from 1.2x previously). Key catalysts include a prolonged disruption in the Straits of Hormuz, which could exacerbate feedstock shortages for naphtha-based competitors and drive further price spikes, while the primary downside risk remains a swift reopening of trade routes that could normalize supply and pressure margins.

In the automotive and manufacturing sector, BYD Company is reportedly reassessing its plans to establish a completely knocked down (CKD) assembly plant in Tanjung Malim, Malaysia. The reconsideration follows new regulatory conditions imposed by the Ministry of Investment Trade and Industry (MITI). These include requirements that 80% of production be exported, while only 20% can be sold domestically at a minimum price threshold of RM200,000. These conditions are aligned with Malaysia’s broader industrial policy objectives, including the National Automotive Policy and the New Industrial Master Plan 2030, which aim to protect domestic automotive players such as Proton and Perodua while promoting higher value-added activities. While BYD had previously secured an interim manufacturing licence in September 2025, the stricter conditions may affect project viability and delay investment decisions. The key implication is a potential slowdown in Malaysia’s ambition to position itself as a regional electric vehicle hub, although this is balanced against the government’s priority to safeguard local industry. From a financial perspective, BYD operates with relatively strong margins for an EV manufacturer, with net margins generally in the mid-single-digit range, supported by scale and vertical integration.

Gas Malaysia Berhad (GMB) is poised for stronger earnings growth supported by regulatory and market-driven tailwinds, prompting an upgrade to BUY with a higher target price of RM5.70 (from RM4.60). Under the Regulatory Period 3 (RP3), the Natural Gas Distribution System (NGDS) base tariff will increase by 19.5% to RM1.880/GJ/day, with an additional surcharge of RM0.234/GJ/day bringing the total allowed tariff to RM2.114/GJ/day in 2026, thereby ensuring a fair return on its expanding regulated asset base and supporting both earnings and cash flow while reducing receivables. Additionally, GMB stands to benefit from rising oil prices, as the Malaysia Reference Price (MRP) for gas is linked to Brent crude on a lagged basis; every US$10/bbl increase in Brent is estimated to boost net profit by RM22–23 million, driven by its gas shipping arm operating under a cost-plus model. Looking ahead, GMB is a strong contender for the new Regasification Terminal (RGT) project, with potential to transform into an integrated midstream player; the project could add RM0.23–0.58 per share to fair value based on an 8–10% IRR and US$500 million capex. Earnings forecasts for FY2027–2028 have been raised by 4–5% on higher MRP assumptions, reinforcing a positive earnings trajectory supported by tariff uplift, oil-linked pricing, and potential project wins, which collectively serve as key catalysts for further valuation re-rating.

Outlook

Malaysia’s economic outlook for March 2026 remains broadly stable, supported by strong industrial activity, resilient domestic demand, and a solid external reserve position. However, downside risks are rising due to external factors, including global energy price volatility and potential trade frictions with the United States. Policy responses, particularly in managing fuel subsidies and maintaining macroeconomic stability, will be critical in navigating these challenges in the coming months. We will continue, favouring companies which demonstrate low valuations, low leverage, high growth, robust management and a strong track record.

INDONESIA

Market Summary

The Jakarta composite Index was down 14.42% month-on-month to close the month of March 2026 at 7,048.22 points. YTD, the index was down 18.49. The Indonesian Rupiah depreciated 1.49% in March against the USD, and closed at IDR17041 for the month.

Economic News

Bank Indonesia maintained the benchmark interest rate at 4.75% at its March policy meeting, in line with market expectations. The decision aims to bolster the stability of the Rupiah while keeping inflation within the central bank’s 2026–2027 target of 2.5% ±1%. Despite global headwinds, the central bank maintained its economic growth forecast of 4.9%–5.7% for 2026.

Retail sales accelerated to 6.9% YoY in February (from 5.7% in January) driven by food & beverages and household equipment spending, with the Ramadan season lifting monthly growth to +4.4% MoM. The Consumer Confident Index softened to 125.2 (from 127), reflecting weaker sentiment among lower- and upper-income households on income and job prospects, while middle-income confidence edged up on improved job outlook.

Indonesia’s trade surplus shrank to USD0.95 bil in January from USD3.49 bil last year. Exports grew 3.39% YoY to USD22.16 bil with non oil and gas exports increased 4.4% but oil and gas exports seen 15.6% YoY drop on lower crude oil and natural gas shipments. Imports grew 18.2% YoY to USD21.2 bil.

Inflation number CPI was higher than expected at 4.8% in February vs 3.5% in January. On a month on month basis, CPI rose 0.7%. Core inflation increased to 2.6%, led by higher gold prices. Mandiri forecasted higher upside risk to current 2026 forecast of 2.8% from rising energy prices due to Middle East tensions.

Indonesia S&P Manufacturing PMI rise to 53.8 in February 2026 from 52.6 in January 2026. It was the highest in the past 2 years, and 7 straight month of expansion. New orders grew for 7th month.

Corporate News

Chandra Asri (TPIA) has declared “force majeure” following disruptions to feedstock shipments through the Strait of Hormuz amid escalating conflict in the Middle East. As of 9M25, the company had approximately USD3.2bil outstanding loan. The net debt is lower at USD1.2bil. The company later clarified that the force majeure is a preventive administrative step, with operations currently running normally while the company manage supply through feedstock diversification and inventory control.

PT Daya Intiguna Yasa MDIY reported 4Q25 revenue of Rp2.2 tril (+15% YoY, +5.5% QoQ), supported by 72 net store opening, bring year end store count to 1226 (+27.6% YoY, +6.2% QoQ), more than offset the softening quarterly same store sales growth SSSG of -9% YoY. Average revenue per store dropped 10.4% YoY. In 2025, revenue increased 16.7% YoY, while SSSG was -7.6%. Management attributed declining SSSG trend to softening consumer confidence, resulting in lower store traffic while basket size remained stable. Net profit in 4Q25 increased 10.2% while the net profit in 2025 increased 3.3%. Management reiterated its commitment to its expansion plan, targeting 270+ new store openings in 2026, balanced between Java and ex Java regions.

Bank of Central Asia BBCA earnings grew 3% YoY in 2M26 to Rp9.2 tril, in line with expectation. Loan grew 6% YoY while deposit grew 10% YoY in 2M26. Loan to deposit LDR ratio dropped to 77.5% from 80.5% a year ago. Net interest margin NIM declined to 5.6% in 2M26 from 6.1% in 2M25. Provision expenses declined 19% YoY in 2M26, resulting in improving credit cost to 0.3% vs 0.4% last year.

PT Industri Jamu dan Farmasi Sido Muncul SIDO sales grew 4% YoY in FY2025. Herbal sales was flat (ASP increase offset softer demand), but the gross profit margin GPM was down 2.2 percentage point due to new product launching. Food and beverages F&B sales were up 12% on both ASP increase (6-8% increase in milk product, 8-10% increase in coffee product) and volume growth. Energy drink grew low teens YoY on strong mining, plantation and construction activities. SIDO target 5-8% sales growth in FY2026 with F&B segment expected to grow double digit. No broad based ASP increase planned. The management cautioned that sales in may fluctuate in 1H2026 due to channel inventory optimization for Tolak Angin.

Outlook

On 28th February 2026, US-Israel started a war with Iran. As of end of March, there is no sign of cease fire in the near term. The effective closure of Straits of Hormuz had sent the Brent crude oil prices above USD100 per barrel. As Indonesia is an oil importing country, the government is actively negotiating with Iran to allow the flow of oil to Indonesia, expedite the B50 biodiesel program. The government also limit the usage of subsidized fuel to control budget deficit. The war will inevitably slowdown the global economy including Indonesia and may negatively impact the Indonesia market. Nevertheless, we are positive on the long term prospect of Indonesia and view the pullback as an opportunity to invest in fundamentally strong company. The LQ45 index is trading at a P/E ratio of 11.8x, below its 5 year mean of 15.4x.

SINGAPORE

Market Summary

The FSSTI Index decreased 2.19% month-on-month to close the month of March 2026 at 4,885.45 points. YTD the index has increased 5.15%. The SGD depreciated 1.72% month-on-month against the USD, and closed at SGD 1.29 for the month of March. YTD the SGD has depreciated 0.11% against the USD.

Economic News

Singapore’s seasonally adjusted unemployment rate held at 2% in Q4 2025, confirming preliminary estimates and unchanged from the previous period. Resident unemployment remained at 2.9%, while the unemployment rate for citizens was stable at 3%. Singapore’s annual inflation rate edged lower to 1.2% in February 2026, from a thirteen-month high of 1.4% in the previous month. The main downward pressure came from housing and utilities (0.3% vs 1.7% in January), driven largely by softer prices in utilities and other fuels.

Singapore’s 10-year government bond yield fell to around 2.23% in late March, retreating from an almost three-month high as demand for local bonds increased. Singapore’s bonds have emerged as a regional haven amid Iran-related turmoil, outperforming other Southeast Asian peers. While the city-state’s economy faces headwinds from rising energy costs and supply chain disruptions linked to the Middle East conflict, strong domestic liquidity and a resilient currency have helped its AAA-rated bonds remain relatively stable. Meanwhile, economists expect the Monetary Authority of Singapore to tighten monetary policy next month and possibly later in the year as rising import pressures weigh on the trade-dependent economy. The MAS will also update its inflation outlook at the meeting, which is currently projected to average between 1%and 2% in 2026.

Corporate News

Sheng Siong (SSG SP) operates the third-largest supermarket chain in Singapore, catering to the mass market with 87 stores located in suburban areas as of FY25. Sheng Siong is rated BUY by RHB with a raised target price of SGD 3.02, supported by strong FY25 results where revenue and earnings grew 10% and 9% YoY respectively to SGD 1.6bn and SGD 149m. The company’s growth outlook is robust, driven by a record 12 new stores opened in FY25 that are set to contribute full 12-month earnings from FY26, alongside an anticipated acceleration in same-store sales growth. With FY26F earnings forecast to jump 24.3% to SGD 185m, RHB has re-pegged its valuation to 25x FY26F P/E,closer to the sector’s long-term average, in anticipation of positive fund flows lifting valuations over the medium term. The stock remains a resilient defensive play targeting the value segment, well-positioned to benefit from consumer down trading, despite a slight 2% ESG discount applied due to its 3.0 score trailing the country median.

Coliwoo Holdings (COLIWOO SP) is Singapore’s market-leading co-living operator, providing a modern housing concept where individuals or groups share communal living spaces while having their own fully furnished, self-sufficient private units. The company’s aggressive growth thesis remains fully intact as it actively recycles capital, having just launched a massive portfolio sale of seven freehold assets with a combined guide price of SGD218.5m at an attractive c.3.5% gross yield. Simultaneously, Coliwoo is executing strategic inorganic growth by acquiring the Park Avenue Changi Hotel for SGD101m, injecting a maximum SGD10m capex to convert it into a 368-room co-living powerhouse targeting a stellar c.20% internal rate of return (IRR). Boasting a highly resilient 1QFY26 portfolio occupancy of 96.5% and projected to double its net profits by FY28F, RHB strongly reiterates a “BUY” rating with a target price of SGD0.82, implying a massive 57.7% upside alongside a c.4.1% dividend yield and FY26 P/E of 9.7x.

Nam Cheong (NCL SP) is a Singapore-listed offshore support vessel (OSV) provider based in Sarawak, Malaysia, principally involved in vessel chartering and shipbuilding. The company is setting a course for a massive multi-year growth phase, prompting RHB to initiate coverage with a strong “BUY” rating and a target price of SGD2.05, implying a 52% upside. Nam Cheong holds a major competitive advantage with its highly attractive young fleet of 36 vessels averaging just9 years old, significantly lower than the aging industry average of 14-16 years. Earnings visibility is highly secured, with a massive MYR1.7bn order book and 64% of its fleet locked into long-term charters. Furthermore, the company just secured its first shipbuilding contract in over a decade, a USD64.5m (c.MYR258m) deal to deliver four OSVs to ADNOC, which will further accelerate top-line growth. Anchored as a strategic Sarawak play that is well-insulated from the ongoing PETRONAS-Petros dispute, analysts project a highly robust 3-year core earnings CAGR of 15%. The stock is currently trading at a deeply discounted c.8x forward P/E, well below the peer average, with 11x FY27F target P/E.

Outlook

The Singapore equity market is transitioning into a consolidation phase after a stellar 2025, where the EQDP (Equity Market Development Programme) successfully re-rated the STI by 22.67%. Currently trading at a 2026 forward P/E of 15x, slightly above its 10-year median of 14x—the market’s valuation reflects a premium for the stability provided by the “Big Three” banks and their attractive dividend yields. However, with GDP growth expected to moderate from a robust 5% in 2025 to a more sustainable 2%-4% in 2026, the focus has shifted from broad-based momentum to selective quality. Given the heightened geopolitical risks in the Middle East and the uncertainty of the US rate cycle, a cautious but opportunistic stance is prudent. The alpha in this environment lies in “deep value” plays: companies with low leverage, resilient earnings growth, and proven management teams that can navigate a cooling macro environment while maintaining solid long-term track records.

THAILAND

Market Summary

The Thai SET Index declined 5.24% month-on-month to close the month of March 2026 at 1448.14 points. YTD the index has gained 14.96%. The Thai baht appreciate 5.15% month-on-month against the USD, and closed at 32.64 THB for the month of March.

Economic News

The Thailand Manufacturing PMI bounced back to 53.5 in February 2026, recovering from last month’s low. This steady climb was sparked by a solid jump in new orders and higher demand, leading to faster output. While manufacturers ramped up buying to restock, employment dipped despite more work piling up. Interestingly, input costs slowed down, but selling prices hit a five-year high.

Thailand’s consumer confidence index, compiled by the University of the Thai Chamber of Commerce, rose to 53.7 in February 2026 from 52.8 in January, marking the highest level since last May. The improvement was supported by the central bank’s rate cut to 1% and expectations of stimulus from a new government after last month’s elections.

Thailand’s exports grew 9.9% year-on-year to USD29.44 billion in February 2026, slowing from 24.4% in January and below expectations due to softer external demand amid Middle East tensions. Growth was supported by industrial products, while agricultural exports declined.

Meanwhile, imports surged 31.8% year-on-year to USD32.27 billion, driven by strong domestic demand, higher purchases of capital goods, raw materials, and gold, supported by government stimulus measures during the election period. As imports outpaced exports, Thailand recorded a trade deficit of USD2.83 billion in February 2026, with a cumulative deficit of USD6.14 billion for January–February 2026.

Thailand’s domestic car sales declined 2.17% year-on-year to 48,282 units in February 2026, reversing the strong growth seen in January and marking the first contraction since March 2025. The slowdown was attributed to weaker economic conditions, tighter auto loan approvals, delayed consumer purchases, and higher energy costs, alongside rising uncertainties from Middle East tensions. By segment, battery electric vehicle sales fell 18.56%, while pickup truck sales declined 1.41%, although early signs of stabilisation are emerging. Meanwhile, car production increased 3.43% year-on-year to 117,952 units, supported by export demand and a gradual recovery in pickups. Car exports remained broadly flat at 81,195 units, with resilient Middle East demand partly offset by shipment delays due to security concerns around key trade routes.

Corporate News

BGRIM’s post-4Q25 analyst meeting with a negative view. Management flagged risks from the latest Middle East conflict, which may lift crude oil and LNG prices. Higher LNG prices would raise domestic gas costs and pressure margins of gas-fired plants. To mitigate tariff mismatch risk seen in 2022–23, they are negotiating with clients covering 200MW (15–20% of IU load) to shift from Ft-based to gas-linked pricing. Vietnam’s 500MW solar tariff remains unresolved, with Bt900mn receivables from EVN, a key overhang. Positively, the Korea wind project (70% complete) targets mid-year COD, and 96MW data centre capacity is secured. While long-term prospects remain intact, every USD1 LNG increase may cut profit by 6–7%. Kasikorn analyst downgrade to Neutral with unchanged TP of Bt15 (DCF, WACC 5.7%).

Charoen Pokphand Foods (CPF) reported 4Q25 net profit of Bt1.09bn (-74% YoY, -79% QoQ). Excluding one-offs, core profit was Bt178m (-97% YoY, -97% QoQ), well below expectations of Bt2.0–2.2bn. The miss was due to weaker GPM, lower share of profit and higher SG&A-to-sales. Gross margin fell to 12.7% (vs 15.7% in 4Q24 and 16.5% in 3Q25) amid weaker livestock performance. Share of profit dropped to Bt1.6bn (-58% YoY, -24% QoQ), mainly from China swine losses. SG&A-to-sales rose to 9.7%. Domestic and Vietnam swine prices are improving, supporting 1Q26 QoQ recovery, though China remains below breakeven. Raw material costs are stable. CPF declared a Bt0.25 dividend (1% yield), XD 8 May 2026. UOBKayhian analyst maintain hold with a lower target price of Bt21 based on 2026 EPS to reflect the softer earnings outlook. Meanwhile, swine prices in Vietnam and China declined further after Chinese New Year.

Land and houses (LH) posted 4Q25 core net profit of THB717m (-8.8% QoQ, -29.3% YoY), 20–27% below estimates due to weaker low-rise transfers, lower residential margin and THB97.6m project provision. FY25 core profit fell 23.5% YoY to THB3.9bn (94% of forecast). A final DPS of THB0.12 was declared, bringing total 2025 dividend to THB0.25 (80% payout). 1Q26F presales are estimated at THB3bn (-17.6% YoY) amid soft sentiment and high-end competition. FY26F presales may miss target. 1Q26F profit is expected flat QoQ but -14% YoY. 4Q26F should be strongest, driven by condo transfers and potential asset divestment gains. CGS analyst maintain Hold with higher SOP-based TP of THB4.12.

Synnex presents a promising outlook following its March 2026 analyst meeting, with management targeting Bt53bn in revenue 12% year-on-year increase. This growth is driven by a robust smartphone replacement cycle and the highly anticipated launch of the MacBook Neo, priced competitively at Bt19.9k. Despite global DRAM shortages, Synnex maintains a stable 4% gross profit margin, bolstered by strong demand for Samsung and Huawei products. Currently, kasikorn’s analyst stock is rated Outperform with a Bt11.86 target price. Trading at a 9.4x PER with a 5.6% dividend yield, SYNEX offers an attractive entry point compared to its peers. While recessionary risks persist, the company’s resilient enterprise segment and strategic inventory management position it as a top contender in the gadget sector.

Outlook

The outlook for Thailand in 2H2026 remains Neutral as geopolitical risks, specifically US-Iran tensions, threaten to spike oil prices, fuel inflation, and weaken the Baht. While a new government arriving in mid-April may launch targeted measures like the “Half-half Plus” scheme, large-scale stimulus is unlikely since public debt is nearing its 70% statutory ceiling. Furthermore, with the policy rate at 1.0% against the Fed’s 3.75%, the Bank of Thailand has no room for further cuts. As corporate expansion slows, many firms are shifting focus toward higher dividend payouts. Consequently, we expect upstream energy and petrochemicals to outperform due to elevated pricing, while sectors sensitive to fuel costs and weak discretionary demand will likely lag behind the SET Index.

PHILIPPINES

Market Summary

The PSE Index decreased 10.02% MoM to close the month of March 2026 at 5,948.94 points. YTD the index has declined to 1.72%. The Peso depreciated 5.34% MoM against the USD, and closed at PHP 60.74.

Economic News

The government took a proactive stance in addressing energy security concerns following heightened geopolitical tensions in the Middle East. President Ferdinand Marcos Jr. approved the release of ₱20 billion from the Malampaya Gas Fund to finance an Emergency Energy Security Program. This initiative aims to safeguard fuel supply continuity and mitigate the impact of global oil price volatility. PNOC Exploration Corporation has been tasked with procuring fuel using these funds to stabilize domestic supply, particularly for critical sectors. Meanwhile, the Department of Trade and Industry is closely monitoring the potential pass-through effects of higher energy costs on essential goods, highlighting risks of broader inflationary pressures.

On the external front, the country’s trade position showed improvement. The trade deficit narrowed to USD4.0 billion in January 2026 from USD4.9 billion a year earlier, supported by a combination of stronger exports and declining imports. Export performance was driven primarily by electronics, which grew by 18.8% year-on-year and accounted for more than half of total outbound shipments, reflecting sustained global demand for semiconductors. Imports declined by 3.1% year-on-year, largely due to reduced purchases of mineral fuels, indicating both softer domestic demand for energy and possible substitution effects amid elevated prices.

Domestic price indicators suggest a gradual build-up of inflationary pressures. Producer prices rose by 1.5% year-on-year in January 2026, accelerating from the previous month and reaching the highest level since mid-2023, indicating rising cost pressures at the production level. Headline inflation also edged up to 2.4% year-on-year in February 2026, remaining within the target range set by the Bangko Sentral ng Pilipinas. However, forward-looking indicators point to a further increase, with March inflation projected to range between 3.1% and 3.9%, and some early estimates suggesting a spike to around 4.4%, driven primarily by non-core components such as energy and transport.

Despite these inflationary pressures, economic activity in the manufacturing sector remained robust. The S&P Global Philippines Manufacturing Purchasing Managers’ Index (PMI) rose to 54.6 in February 2026, up from 52.9 in January. This expansion reflects stronger new orders and the fastest pace of output growth since November 2018, indicating sustained momentum in the industrial sector and continued business confidence.

In terms of regional engagement and investment promotion, the Philippines is actively preparing for its 2026 ASEAN Chairmanship. The government, through the Department of Trade and Industry in collaboration with the Asian Development Bank, is organizing the ASEAN Business and Investment Summit (ABEF 2026). This initiative is expected to enhance the country’s investment profile and attract foreign direct investment inflows by showcasing economic opportunities across key sectors.

Efforts to strengthen energy resilience are also progressing through the expansion of renewable energy capacity. The Department of Energy is accelerating the development of 1,471 MW of renewable energy projects to address potential supply constraints. In parallel, MTerra Solar has contributed an additional 250 MW of solar capacity and 450 MWh of energy storage to the national grid, supporting the country’s transition toward a more sustainable and diversified energy mix.

Overall, while the Philippines continues to demonstrate resilience through strong manufacturing activity and improving trade dynamics, near-term risks remain tilted to the upside for inflation, largely driven by external energy shocks. Government intervention and ongoing energy diversification efforts will be critical in mitigating these risks and sustaining economic stability.

Corporate News

In the energy sector, Petron Corporation indicated that its fuel inventory remains sufficient until June 2026, supported by the procurement of Russian crude oil. This move reflects a strategic effort to secure supply amid elevated global oil prices and geopolitical uncertainties. Petron’s business model, which is highly sensitive to input cost volatility, typically operates on thin refining margins, often in the low single-digit range, given the pass-through nature of fuel pricing. The near-term catalyst lies in inventory cost advantages and timing gains, as lower-cost sourced crude could support margins if retail prices remain elevated. However, sustained high global oil prices and currency depreciation may continue to pressure working capital and financing costs.

In the retail sector, Robinsons Retail Holdings Inc. (RRHI) is undergoing a significant corporate restructuring. A voluntary delisting has been proposed by its parent, JG Summit Holdings, through a tender offer via JE Holdings, resulting in a trading suspension on March 27, 2026. This move suggests a strategic shift toward privatization and operational flexibility, allowing the group to streamline decision-making and pursue long-term restructuring without public market pressures. Concurrently, the closure of all 11 “No Brand” stores in the Philippines by June 2026 reflects a recalibration of its retail portfolio, likely due to subscale operations and margin dilution. RRHI historically operates on low net margins (approximately 2–4%), typical of the grocery and mass retail segment. The key catalyst post-delisting will be margin improvement through cost rationalization and portfolio optimization.

Megaworld Corporation, one of the Philippines’ leading township developers, reported 4Q25 core earnings of PHP5.0bn (-19% YoY, -10% QoQ) due to weaker residential bookings and lower ready-for-occupancy (RFO) sales, bringing FY25 core earnings to PHP20.9bn (+5% YoY), broadly in line with expectations. Residential presales softened to PHP27.7bn (-6% YoY, -19% QoQ) amid subdued property sentiment, although unsold inventory remained healthy at PHP135bn (13.9 months of supply) with PHP103bn in unbooked revenues providing earnings visibility. Meanwhile, the leasing segment remained resilient with office revenue at PHP3.8bn (flat YoY, +3% QoQ) and stable occupancy of 87%, supported by demand from non-voice BPOs and global capability centres. Looking ahead, the company plans to accelerate the expansion of MREIT, Inc., targeting 1 million sqm of gross leasable area, which is expected to drive capital recycling of at least PHP5bn annually and improve free cash flow generation. This strategy could lift FY26–27 FCF to PHP1.6bn–PHP1.8bn, supporting stronger shareholder returns through dividends. The debt-to-equity is estimated at 33.1% for FY2026, with a dividend yield of 4.8%, and FCF is expected to improve.

JG Summit Holdings Inc. remains a compelling long-term BUY, underpinned by resilient core earnings and attractive valuation despite near-term volatility. Core net income (excluding one-offs) rose 3% YoY to PHP31.9bn, beating expectations by 15%, although reported earnings swung to a loss of PHP87.9bn due to a one-off PHP114.3bn impairment from JG Summit Olefins Corp., whose operations were halted to stem losses. Revenue grew 9% YoY to PHP368.6bn, supported by strong performances from Cebu Air (passenger volume +10% YoY to 26.9mn) and Robinsons Land (rental income +10% YoY to PHP13.9bn), highlighting the strength of its diversified portfolio. While FY26 earnings may face headwinds from elevated jet fuel costs and a weaker peso, estimated to reduce Cebu Air’s profit by around PHP2.1bn. This is partially offset by longer-term catalysts such as Meralco’s MTerra solar project contributing from 2027. At PHP26.20/share, JGS trades at a deep 36% discount to its PHP40.63 target price and at an undemanding 6.15x 2026F PER (vs. 6.67x sector average), offering an attractive entry point for investors seeking value with cyclical recovery and infrastructure-driven upside.

Outlook

PSEi Composite Index remains cautious in the near term, with a downside bias driven by external headwinds, particularly the ongoing Middle East conflict, which continues to exert upward pressure on global oil prices. As a net energy importer, the Philippines faces rising inflation risks that could limit policy flexibility for the Bangko Sentral ng Pilipinas and keep interest rates elevated, weighing on equity valuations. At the same time, a weaker peso and higher fuel costs are likely to compress corporate margins, especially in import-dependent sectors. While resilient domestic demand and improving manufacturing activity provide some support, the market is expected to remain volatile and range-bound. We will continue to favouring defensive and fundamentally strong companies with rising profits, good management and low gearing levels amid ongoing global uncertainty.

SOUTH KOREA

Market Summary

The KOSPI index closed the month of March at 5,052.46 points, declining 19.08% MoM.

Economic News

Korea’s industrial output posted its fastest growth in five years and eight months in February, mainly driven by gains in semiconductor production. Industrial production rose 2.5 percent from a month earlier last month, according to the data from the Ministry of Data and Statistics. It marked the fastest increase since June 2020, when output jumped 2.9 percent mom. Output in the mining and manufacturing sector, a key pillar of the economy, advanced 5.4 percent mom in February. This marked the steepest gain since June 2020, when the figure rose 6.6 percent. Notably, semiconductor production surged 28.2 percent from a month earlier, as global demand continued to grow amid the artificial intelligence (AI) boom. Chip output increased by the most since January 1988, when production rose 36.8 percent mom. The semiconductor production index also reached a record high of 215.4, surpassing the previous record of 211.6 set in September last year. Output in the electronics and telecommunications sector also jumped 20.9 percent, the steepest mom increases since January 2009, when it rose 24.7 percent.

Banks’ overall lending rates rose for the fourth consecutive month in February, driven by higher mortgage loan rates amid tighter regulations aimed at stabilizing the housing market. The average interest rate on new bank loans stood at 4.26 percent last month, up 0.02 percentage point from January, according to the data from the Bank of Korea (BOK). The figure has increased steadily since November 2025. The average rate on corporate loans rose 0.05 percentage point to 4.2 percent. The rate on new household loans, however, fell 0.05 percentage point to 4.45 percent, marking the first decline in five months, mainly due to a reduced share of unsecured loans with relatively high interest rates. But the average rate on mortgage loans edged up 0.03 percentage point to 4.32 percent, reaching the highest level since November 2023 as stricter rules on home purchase loans remained in place to cool the overheated property market and rein in household debt. At its latest rate-setting meeting late last month, the central bank kept its benchmark interest rate unchanged for the sixth consecutive meeting.

Corporate News

Korea Aerospace Industry (KAI) delivered 4Q25 Sales of W1.5tn (+34% yoy/+108.9% qoq), the latter missed consensus by 30%. The worse than expected 4Q25 earnings was attributed to one-off repair cost of W24.5bn. The new order and earnings will improve in 2026 amid the shift into mass production cycle. KF-21 mass production is starting in full-scale, and domestic rotary wing volume will expand. The completed product exports will rise for Poland and Malaysia, and the delayed exports volume from 2025 will be delivered in 2026, leading to 60 units of aircraft delivery vs. 15 in 2025. The additional new order momentum is also expected in SE Asia (KF-21), while US navy project’s trainer aircraft bidding will also begin. Given KF-21 is KAI’s next generation product, it is the beneficiary from expanding defense budget in US. KAI shared its 2026 guidance at sales/new order growth of 55% and 63%. Separately, the company announced to issue CB of W500bn in order to ease the temporary burden of working capital and investment for the future project. The CB interest rate is set at 0%, while the conversion price is W185,165.

Samsung SDI delivered 4Q25 Sales of W3.9tn (+2.8% YoY/+26.4% QoQ) and operating loss (OP) loss of W299.2bn (turned red YoY and QoQ), the latter was inline with the market consensus. The xEV battery division losses shrunk from increased compensation payment from the client, while subsidy figure (APMC) came out stronger than expected at W60.7bn (with JV ESS shipment forecast of 5GWh) from weakened KRW vs USD. For 2026, the xEV shipment is expected to grow high single digit percentage from the client’s new model project, and energy storage system (ESS) to grow +50% yoy from expanding AI data center market. The ESS division’s profitability to improve meaningfully from 2H26, due to more allocation to local mass production in the US, thus less tariff impact and more tax deduction. The small battery division’s loss is expected to improve led by rising power tool and BBU demand from data center construction.

Outlook

Korea remains on our watch list as a potentially attractive investment destination. The focus will remain on stock selection. We continue to look for opportunities in the region, favouring companies which demonstrate low valuations, low leverage, high growth, robust management and a strong track record. At present, we like the memory, renewable energy and domestic consumption industry.

HONG KONG & CHINA

Market Summary

The CSI-300 Index declined 5.53% in March to close at 4,450.05 points. The Hang Seng Index declined 6.92% in March to close at 24,788.14 points.

Economic News

The 2026 Two Sessions meeting on 5th of March 5. The 2026 Government Work Report sets key economic and social goals, lowering the growth target from 5% in 2025 to 4.5%-5%. The adjustment aims to allow 2026 economic policies to focus more on improving growth quality while creating room for structural adjustments, reforms, and risk prevention. In practice, to ensure a strong start to the 15th Five-Year Plan, efforts are expected to be directed toward mid-range growth within the target range. The 2026 Government Work Report places greater emphasis on the price level, aiming to turn the GDP deflator from negative to positive. This suggests that measures to regulate overall supply and demand may become more proactive. Fiscal and monetary policies balance supporting economic growth, promoting structural adjustments, preserving future policy flexibility, and enhancing coordination. Fiscal policy will play a more direct role in boosting domestic demand, with new government bonds totaling RMB11.89trn in 2026, slightly higher than the RMB11.86trn in the 2025 budget. However, the share of new government bonds to GDP will decrease from 8.5% in 2025 to 8.1% in 2026.

China’s exports surged 21.8% YoY in 2M26, after expanding 6.6% in last December, far exceeding the market consensus. Meanwhile, imports also surprisingly grew 19.8% in 2M26 after rising 5.7% in December. The distortion of Spring Festival, recovering global manufacturing activities and diversified trade regional structure boosted the robust exports in 2M26. The recent rising US-Iran geopolitical conflicts and the block of the Strait of Hormuz are expected to weigh on the exports to the Middle East region. The exports growth is expected to moderate in March after the strong start of 2026, reflecting the high base in last March and the encumbrance of recent geopolitical conflicts. However, the products competitiveness in equipment manufacturing industries and the diversified regional trade landscape will continue to sustain the resilience of exports’ performance.

Corporate News

361 Degrees delivered another year of solid performance, marking its fifth consecutive year of double-digit revenue growth. FY25 revenue rose 10.6% YoY to RMB11.1bn, while net profit increased by 14% YoY to RMB1.3bn, in line with market expectations. Profitability was supported by improved operational efficiency while advertising and promotion expenses as a percentage of revenue declined by 230bps to 10.5%. Meanwhile, operating cash flow surged 10.7x to RMB815bn, reflecting significant improvements in receivables and inventory management. The company announced a final dividend of 31.7 HK cents per share, translating it to a full-year payout ratio of 45% and a yield of approximately 6%, highest in the sportswear segment. There is strong potential from overseas markets. International operations delivered outstanding performance, with overseas retail sales revenue surging 125% YoY. At the end of 2025, there were 1,253 overseas outlets, accounting for about 19% of the total 6,647 POS. Cross-border e-commerce sales revenue doubled YoY. The management indicated that overseas business and cross-border e-commerce will be the key incremental growth drivers in FY26. By channel, e-commerce revenue grew 25.9% YoY (vs. 12.2% YoY in the prior period), reaching RMB3.29bn and accounting for approximately 30% of total revenue, up 360bps YoY. Its direct-to-customer strategy has expanded to instant retail platforms such as Meituan Flash Buy and Taobao Flash Sale. The company plans to expand instant retail coverage to more cities. “Super Premium Store” shows promising growth – Launched in 2025, the company’s new “Super Premium Store” format had 127 POS by the end of 2025, with an additional 12 opened so far in 2026. The management targets 100 new openings in FY26. Currently, more than 80% of existing Super Premium Stores are already profitable.

Xiaomi’s 4Q25 results were broadly in line. Revenue reached RMB116.9bn, up 7.3% y/y, while adjusted net profit fell 23.7% y/y to RMB6.35bn; both were broadly in line with consensus. Group gross margin was maintained at 20.8%, up 0.2ppt y/y, as stronger profitability in smart EV partly offset sharp margin pressure in smartphones and softer IoT demand. By segment, smartphone revenue declined to RMB44.3bn (-13.6% y/y), with shipments down 11.6% (vs. consensus of -13.5%) and ASP down 2.2%. Smartphone gross margin fell 3.7ppt y/y to 8.3% (vs. consensus of 8.8%), from 12.0% in 4Q24 and 11.1% in 3Q25, mainly because of significant DRAM and NAND price hikes and intense competition. IoT and lifestyle revenue declined to RMB24.6bn (-20.3% y/y), hurt by subsidy normalisation and weaker large home-appliance demand in China, while IoT gross margin slipped to 20.1% from 23.9% in 3Q25. Internet services remained resilient, with revenue reaching a record RMB9.9bn (+5.9% y/y) and gross margin stable at 76.8%, supported by advertising and ecosystem expansion. The standout remained smart EV, AI and other new initiatives. Segment revenue rose to RMB37.2bn (+123.4% y/y), driven by 145,115 vehicle deliveries (+108.2% y/y). Segment gross margin improved 2.3ppts y/y to 22.7%, and operating income reached RMB1.1bn. Total EV deliveries reached 411,082 in FY25. Looking at the broader business, Xiaomi continued to make progress in premiumisation and ecosystem expansion.

Outlook

We are becoming more optimistic on China’s economy given potential policies support to maintain growth and stability. The current challenges to revive economic activities and investors’ confidence are facing headwinds. Valuation is also becoming more attraction. We think it is necessary for the Chinese government to address the structure imbalances for a more balance and sustainable recovery. At present, the regulatory environment focuses on social stability over growth. We continue to favour companies with robust fundamentals, low valuations, good management, and low leverage.

TAIWAN

Market Summary

The TWSE index closed the month of March at 31,722.99 points, declining 10.42% MoM.

Economic News

Taiwan’s economic monitoring indicator flashed a red light for the third straight month in February, with the composite score rising to its highest level in more than four years according to the National Development Council (NDC). The composite index climbed one point from a month earlier to 40, the highest since July 2021, remaining in the red zone that signals an overheating economy. The NDC uses a five-color system to track the economy. A red light (38-45 points) signals overheating; yellow-red (32-37) indicates a warming economy; green (23-31) suggests stable growth; yellow-blue (17-22) reflects sluggishness; and blue (9-16) points to contraction. Of the nine monitoring indicator factors, the sub-index on overtime hours in the industrial and service sectors rose two points to red, driven by strong demand for artificial intelligence applications and Lunar New Year-related distortions. The manufacturing business sentiment indicator fell one point to yellow-blue from green, reflecting fewer working days during the holiday period and more cautious views among firms.

Taiwan export orders reached US$63.88bn in February, down 16.9% MoM (up 1.9% MoM seasonally adjusted) and up 23.8% YoY, slightly below the consensus estimate of 24.5%. ICT for the electronics supply chain outperformed electronics, which in turn outperformed optical components; for traditional industries, machinery benefitted from AI related demand, and plastics & rubber posted the weakest performance. Among major products, ICT export orders were down 9.6% MoM, but up 55.2% YoY to US$22.72bn. The category was largely unaffected by the shift in Lunar New Year timing last year, as aggressive capex expansion by major CSPs drove strong demand for servers and networking equipment, supporting robust order growth. Electronics orders came in at US$26.25bn, down 19.5% MoM but up 26.2% YoY, supported by strong demand for AI and high performance computing (HPC), which boosted orders for IC manufacturing, chip distribution, and memory, though growth was not as broad based as in the previous two months. In terms of geographical mix. Order growth was strongest in the US & ASEAN, while both China & Europe saw YoY declines. Orders from the US rose by 45.1% YoY in February, with ICT products contributing the most to growth in the first two months, up 112.3%, or US$10.4bn. Orders from China and Hong Kong fell by 0.2% YoY, as cumulative January–February orders were primarily driven by electronics orders, which increased by 44.3% YoY, or US$4.88bn. Orders from Europe declined by 5.6% YoY, with ICT products posting the strongest growth in January–February, up 39.4% YoY. Orders from ASEAN and Japan expanded by 33.8% and 17.8% YoY, respectively.

Corporate News

Quanta Computer 4Q25 EPS beat. The 4Q25 EPS of NT$5.76 was up 35% QoQ and 40% YoY, beating the consensus. The gross margin of 6.3% and operating margin of 3.8% were largely in line with estimates driven by the GB300 shipments ramping up. The server sales weighting rose to 75-80% (vs. 70% in 3Q25), while AI server accounted for 75-80% of server sales (vs. 70% in 3Q25), mostly GB shipments. With a stable operating expenses ratio but higher forex gains of NT$3.55bn, 4Q25 EPS was a beat. 2025 EPS reached NT$19.45, up 26% YoY, also better than expected. The company plans a cash dividend of NT$15.6 per share, for a payout ratio of 80%. The company remains positive on AI server sales growth for 2026F, guiding for triple-digit YoY growth (unchanged), with GB, VR and ASIC sales all expanding significantly. Hence, the server sales contribution looks to increase to over 80% this year, with AI server rising to over 80% of total server sales. General server sales grew 30-50% last year, and it expects sales to be only stable this year, as more resources are allocated to the AI business. For notebook business, Quanta maintains guidance that 2026F shipments will track industry trends, likely declining YoY on high consumer model exposure amid memory price hikes, which are hindering demand. For EV, sales fell by double digits last year, with contribution down to low single digits.

Lite-On Technology reported 4Q25 EPS of NT$1.70, below expectation by 7%, mainly on a 4% revenue shortfall to NT$44.3bn, down 1% QoQ, partially due to slower pull-in on memory tight supply. The operating margin arrived in line at 10.5%, while gross margin missed by 2.5% on the financial impact of US tariffs. The firm saw server-related revenue surge nearly 75% YoY to account for 31% of 2025 revenue, while that of other businesses was up 7%. A 2H25 cash dividend of NT$3.00 implies a payout ratio of 80%. The company targets 30%-plus AI revenue weighting in 2026F. Lite-On’s AI sales exposure surpassed 20% in 2025, including 16% from power supply unit (PSU) and 3-4% from battery backup unit (BBU). The firm is a key PSU supplier of three out of the five tier-1 US hyperscalers, and is working extensively with one of these firms in BBU and power rack. The development of 110kW power shelf, the standard for Nvidia’s (US) VR200 rack, remains on track, and the firm aims to gain market share in AI server PSU this year. Lite-On is lifting its capex budget in 2026F to NT$11.0bn, up from NT$6.85bn last year, mainly for capacity expansion in Taiwan, Vietnam and the US. Capex will likely maintain at high levels in 2027F. Shipments of liquid cooling system to a major US server OEM, however, are postponed to 2Q26F.

Outlook

Taiwan remains on our watchlist as a potentially attractive investment destination, the depth of the electronics supply chain present opportunities to identify good companies that are less well-owned compared to the semiconductor sector. We are also exploring investment into non-electronics sector that will benefit from global structural trend. We continue to favour companies which demonstrate low valuations, low leverage, high growth, robust management and a strong track record.

VIETNAM

Market Summary

The Vietnam Ho Chi Minh Stock Index (VNI) fell 10.95% month-on-month to close the month of March at 1,674.49 points. Foreign investors continued net selling throughout the month. The Vietnamese Dong depreciated 1.07% month-on-month against the USD, and closed at 37,965 for the month of March.

Economic News

Vietnam’s trade balance reversed to a deficit of USD 0.67 billion in March 2026 from a surplus of USD 1.70 billion in the same month a year earlier. YoY, exports rose 20.1% to USD 46.44 billion while imports grew faster at 27.8% to USD 47.11 billion. For the first quarter, exports increased 19.1% to USD 122.93 billion, with sales of computers, electronics, and components surging over 40%, while phones and machinery rose 23.1% and 18.2%, respectively. Meanwhile, the agriculture, forestry, and fisheries sector expanded 5.9%. Imports in the period jumped 27.0% to USD 126.57 billion, resulting in a cumulative trade deficit of USD 3.64 billion. International arrivals to Vietnam rose 1.3% year-on-year to 2.08 million in March 2026, marking a sharp slowdown from the 17.7% surge in the previous month. The sharp slowdown came amid rising fuel prices, prompting Vietnamese airlines to scale back operations.

Vietnam’s annual inflation rate accelerated to 4.65% in March 2026 from 3.35% in the previous month, marking the highest level since January 2023 and the fastest March year-on-year CPI increase in the past five years. Upward price pressures were broad-based across most components, including food (4.72% vs 5.28% in February), beverages and tobacco (3.44% vs 3.03%), clothing, hats, and footwear (1.82% vs 1.87%), housing electricity, water, fuel and building materials (5.88% vs 5.60%), household equipment and goods (2.44% vs 2.23%), healthcare (1.0% vs 0.74%), transport (10.81% vs -3.19%), education (3.30% vs 3.21%), culture, entertainment and tourism (2.07% vs 2.31%), and other goods and services (4.01% vs 4.10%). On a monthly basis, consumer prices increased 1.23%, after 1.14% gain in February, the steepest pace since February 2021.

Corporate News

PetroVietnam Technical Services Corporation (PVS) is Vietnam’s leading oilfield technical services provider, offering marine base services, floating storage and offloading (FSO/FPSO) operations, mechanical and construction engineering, and offshore exploration support. PVS operates across Vietnam’s key upstream basins and has expanded its presence internationally across Southeast Asia and the Middle East. The company sits at the intersection of two powerful tailwinds in the current environment. First, the sustained elevation in global oil prices- with Brent at USD109/bbl and WTI at USD112/bbl- directly supports upstream capital expenditure by oil majors and national oil companies operating in Vietnam and the broader region, and consensus expects PVS to benefit from a multi-year cycle of rising offshore project awards as operators seek to maximise output. Second, the Strait of Hormuz disruption has accelerated interest in alternative supply routes and non-Middle Eastern production hubs, increasing the strategic importance of Vietnam’s offshore upstream sector and supporting higher regional oilfield services pricing. The company carries a clean balance sheet with minimal net gearing- a notable differentiator in a sector often characterised by capital-heavy balance sheets- providing PVS with the financial flexibility to participate in large-scale engineering and construction contracts without the financing risk that constrains levered peers. Domestically, PVS is well-positioned to benefit from the Vietnamese government’s push to accelerate upstream development at major fields including Block B and Ca Voi Xanh as energy security concerns intensify. While the timing of large project awards can be lumpy and create short-term earnings variability, the medium-term project pipeline is robust and the current oil price environment provides a supportive backdrop for contract escalation and margin expansion. HSC names PVS as a medium-term outperformer in its energy infrastructure theme. PVS is currently trading at a forward FY26 PE of approximately 12x with a net cash position.

Masan Group (MSN) is one of Vietnam’s largest private conglomerates, operating an integrated consumer-retail ecosystem spanning FMCG, modern retail, processed meat, high-tech materials and financial services under its “Point of Life” platform. In FY25, the group delivered a strong earnings recovery with consolidated revenue reaching VND81.6 trillion (+8.7% on a like-for-like basis) and NPAT post-minority interest surging 105.5% year-on-year to VND4.1 trillion. The result was underpinned by broad-based improvement across segments: WinCommerce (WCM) recorded revenue growth of 18.3% to VND39.0 trillion and swung to NPAT of VND501 billion (up 86.8x year-on-year) as its network expansion- nearly 800 new store openings in FY25, reaching 4,592 outlets- began converting scale into profitability, with like-for-like growth accelerating to 11.3% in Q4. Masan Consumer (MCH) returned to positive revenue growth in Q4, with the Retail Supreme distribution model now covering approximately 420,000 retail outlets as of February 2026 and generating cumulative revenue growth of 15.2% year-on-year in the first two months of 2026, ahead of the full-year guidance of 11–15%. The standout near-term earnings driver is Masan High-Tech Materials (MSR), which is positioned for a “harvest year” as tungsten APT prices have surged from USD518/mtu on average in FY25 to USD1,900–2,500/mtu in early 2026, far exceeding the company’s planning assumption of USD900/mtu — a structural windfall driven by China tightening tungsten exports by 40% amid declining global mine reserves, which makes MSR’s Nui Phao mine one of the few strategically valuable alternative supply sources globally. The principal risk to the FY26 outlook lies in the MEATLife (MML) segment, where recovering hog supply and rising feed costs may moderate near-term profitability, though MML’s deepening integration with WinCommerce contributing 19% of WCM’s animal protein revenue, provides a structural buffer. The balance sheet continues to strengthen, with net debt/EBITDA easing to 2.74x at FYE25. Both JP Morgan (Overweight, TP VND96,000) and Guotai Junan (BUY, TP VND96,198) maintain constructive ratings, with consensus pointing to FY26 EPS growth of approximately 42%. MSN is currently trading at a forward FY26 PE of 19.3x with net debt/EBITDA expected to ease to 2.6x at FYE26.

Vinhomes is the largest commercial real estate developer in Vietnam. Founded as a subsidiary of Vingroup, the company is the second largest public company in Vietnam (behind their parent company VinGroup). VHM reported a strong 4Q25 with PATMI more than doubling YoY to VND 26.7tn (US$1.3bn), bringing FY25 PATMI to VND 41.1bn, which is 7% ahead of Bloomberg consensus. They have multiple projects are ready for launch (Table 2Vinhomes Projects and Launch Pipeline) across Hanoi, Quang Ninh, Da Nang, and HCMC, with timing dependent on market conditions. Revenue contributors in 2026 will include Wonder City, Green City, Golden City, Green Paradise, Ocean Park 2 and 3, and Royal City. With infrastructure works underway at Green Paradise, the retail launch will be instrumental in driving 2026 sales. However, the SBV has maintained a restrictive credit growth cap of 15% for 2026, instructing banks to mirror 2025 levels. This tighter liquidity environment has pushed 12-month fixed deposit rates to the 7-7.5% range (up from ~5.5% in 1H25), with mortgage rates now hovering between 7% and 9%. Despite these headwinds, VHM management remains confident, citing preferential rates secured with partner banks and aggressive buyer incentives, such as 18–36 month payment deferrals. While the company’s net gearing moderated slightly to 37.9% this quarter, it remains significantly higher than 2024 levels due to an intensive ramp-up in construction and development. VHM is currently trading at a forward FY26 PE of 9.80x

Outlook

The near-term outlook for Vietnam’s equity market remains very cautious, with HSC Research estimating the VNIndex is trading at approximately 13.6x trailing P/E- not yet sufficiently cheap to justify aggressive accumulation- and noting that a further correction of approximately 10% to the 1,500 level, implying a valuation of approximately 12.2x or roughly -1 standard deviation to the five-year average, would represent a historically compelling entry point that has only been available four times in the past six years. The dominant macro overhang remains the Strait of Hormuz crisis: Vietnam, as a net energy importer sourcing 78.6% of its crude from Kuwait, is directly exposed to supply disruption risk, and the 132% surge in domestic diesel prices since end-February is already feeding through into March CPI at 4.65% and into transport and logistics cost structures across the economy. The SBV has directed credit institutions to stabilise interest rates, but interbank overnight rates remain elevated at 9–10%, deposit rates have risen sharply since the Tet holiday, and the narrowing US-Vietnam yield differential could amplify capital outflows and reduce the effectiveness of monetary easing as a policy tool. Against this backdrop, market leadership should remain highly selective: domestically-oriented consumer and retail names with pricing power- MSN, MWG and PNJ- are relatively insulated from geopolitical and FX pressures; industrial park developers, which have lagged since April 2025’s tariff announcements, offer an upside anchored by Vietnam’s strong Q1 FDI inflows of USD15.2 billion (+42.9% year-on-year); and energy infrastructure names such as PVS and GAS stand to benefit structurally from elevated oil prices and Vietnam’s accelerated upstream development agenda. The FTSE Russell market review outcome on 7 April represents a near-term catalyst- a positive decision could trigger passive inflows of USD300–500 million during the September rebalancing- though the amount may be insufficient to single-handedly reverse the prevailing bearish trend, and the path to a sustainable re-rating remains contingent on a resolution of the Iran-US standoff and a stabilisation of domestic fuel and funding costs.

Disclaimer:

The above information has not been reviewed by the SC and is subject to the relevant warning, disclaimer, qualification or terms and conditions stated herein. The information is intended for institutional and accredited investors and the recipient should be aware of the securities laws and regulation of your jurisdiction in your review of the material. The material should not be construed as formal investment, legal, tax or accounting advice and such formal advice should be acquired by any individual investor prior to making an investment. The information contained herein does not have any regard to the specific investment objectives, financial situation or particular needs of any person. We assume no responsibility or liability for any errors or omissions in the content of this article.