Market Review October 2025

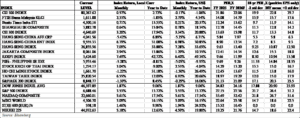

Risk assets strengthened further in September across regions. As expected, the Federal Reserve cut rates by 25 bps in September. The markets reacted positively, registering broad-based gains. The market has also factored in an additional 50 bps of cut for the rest of 2025. The World Index gained 3.09% in September. The MSCI Far East Ex. Japan index continued to chalk up further gain, adding 7.99%, driven by North Asia markets. ASEAN equities performance lagged with a return of +0.11%, after a +2.39% gain in August. Vietnam (-1.22%) and Philippines (-3.28%) stood out with negative returns. Regional currencies mostly weakened against the USD. The best performing currencies were Malaysia Ringgit (+0.42%) and Taiwan NT (+0.35%), while the weaker ones were Philippines Peso (-1.82%) and Korean Won (-1.01%).

The US markets performed well with broad based gains driven by the Federal Reserve’s dovish stance and better than expected Q2 corporate earnings growth. The 12.7% earnings growth for the S&P 500 index stocks far exceeded market expectation of 7.2%. Strong earnings reports reinforced the view that the political turmoil of the past months has so far had only a muted impact on US company earnings, at least for now. The Federal Reserve cut rates by 25 bps in September. The market has also factored in an additional 50 bps of cut for the rest of 2025. Dow Jones Industrial Average (DJIA) and S&P 500 Index and Nasdaq Composite gained 1.87%, 3.53% and 5.61% respectively.

The Stoxx Europe 600 Index added another 1.46% from prior month. The eurozone headline inflation ticked up 2.2% year on year in September, slightly below expectations of a 2.3% rise. The economic sentiment indicator for September reflected cautious optimism. The overall indicator saw a minor increase from 95.3 to 95.5. Consumer confidence also ticked up by 0.6 points to -14.9 (from -15.5), although it remains low by historical standards.

Hong Kong and H shares indices extended their gains in August. For the month of September, Hang Seng Index and Hang Seng China Enterprises Index gained 7.09% and 6.79% respectively, driven by index heavy technology sector on artificial intelligent theme and on relative valuation to global peers. Chinese A shares also gained further, positive return 3.20%. Housing market remained lacklustre, holding back China economy growth strength. China’s existing home prices declined at an accelerated pace in August, highlighting the urgency behind recent easing measures introduced by major cities to revive the struggling property market. Resale home values fell 0.58% from July, quickening from a 0.55% decline a month earlier, according to the National Bureau of Statistics.

South Korea’s KOSPI Index rebounded from the 1.67% decline in August. It gained 7.49% in September, driven by Samsung Electronics over positive outlook on memory sector recovery. South Korean businesses economic conditions improved for the second consecutive month due to recovery in chipmakers and the extra budget plan to bolster consumer demand. The composite business sentiment index (CBSI) in all industries rose 0.6 points over the month to 91.6 in September after going up 1.0 point in August, according to the Bank of Korea (BOK). The continued improvement was attributed to the enhanced industry outlook for semiconductor manufacturers.

Taiwan’s TWSE Index gained 6.55%, after a tepid 0.6% rise in August. The September gain was driven by global technology sector strength. Taiwan export orders continued to show strength. Taiwan export orders totalled US$60.02bn in August, up 19.5% Year-on-Year, beating forecast of 13% Year-on-Year growth and consensus of 12.8% Year-on-Year growth, as the reciprocal US tariff rate increase on August 7 has not yet been applied to Taiwan’s major exports to the US, such as semiconductors and ICT products. On the domestic side, the government has been proactive to boost economic activities. The Taiwan government approved a preferential housing loan program for young people that will exclude them from the restrictions placed on banks’ percentage of real-estate loans under Article 72-2 of the Banking Act. Tight lending rules have slowed mortgage approvals.

Singapore’s STI consolidated, gaining 0.71%, slowing from the 3.51% gain in the previous month. On economic front, Singapore non-oil domestic exports (NODX) slumped 11.3% in August 2025, the steepest decline since March 2024. Non-electronic exports fell 13%, dragged down by food preparations, machinery, and petrochemicals, while electronics dropped 6.5%, reversing July’s growth. Exports to the US, China, Indonesia, and other key markets declined, while those to South Korea, Taiwan, and the EU saw gains. On a monthly basis, NODX fell 8.9%. External demand remained a challenge for the island.

Malaysia’s KLCI gained 2.33%, also slowing from the 5.1% rise in August. Malaysia’s exports eased sharply in August. Export growth fell to 1.9% Year-on-Year in August from 6.5% in July, undershooting expectations and consensus. On a sequential basis, this implies export growth had declined 6.3% Month-on-month after a significant rebound to 20.2% in the previous month. Re-export growth slowed to 22.6% Year-on-Year in August from 41.9% in July, while domestic export growth also deteriorated to -2.5% from -2.3%. Electronics export growth eased to 10.1% Year-on-Year in August from 22.5% in July. The headline inflation rose slightly to 1.3% Year-on-Year in August from 1.2% in July, in line with consensus expectations. On a sequential basis, this implies headline inflation was 0.15% Month-on-month, unchanged from the previous month. Core inflation also edged up to 2.0% Year-on-Year in August from 1.8% in July

Thailand’s SET Index stabilized, gaining 3.04%. Thailand posted a trade deficit of USD 1.96bn in August 2025, reversing from a USD 0.26bn surplus a year earlier and missing forecasts of a USD 0.68bn surplus, marking its first deficit since April as imports outpaced exports. Exports grew 5.8% Year-on-Year to USD 27.74bn, the slowest in 11 months, dragged down by softer US shipments (12.8% vs 31.4%) after the US imposed a 19% tariff. Industrial product exports rose 11.2% (computers +44.1%, ICs +37.0%), while agricultural exports fell 10.7% (fruit, rubber, rice were down).

Jakarta Composite Index gained 2.94%, slowing from the 5.06% rise in August. The government announced interest rate subsidy program for housing loans starting FY26, offering an effective 5% rate per year for suppliers and 10% for the demand side (loan ticket size Rp100mil to 500mil) to further boost economic activities. Indonesia’s fiscal deficit widened to Rp82tril in August (vs Rp35 tril in July), bringing 8M25 deficit to Rp322tril or -1.3% of GDP vs -0.7% in 8M24. The widening of the deficit was due to weaker revenue (-5.9% Month-on-month) and stronger spending (+13% Month-on-month), especially in social programs.

The Philippines PSE Index corrected sharply, dropping 3.28%. Philippines’ budget deficit widened to PHP84.8bn in Aug-2025 from PHP54.2bn a year ago. Revenues rose 11.4% Year-on-Year to PHP352.5bn, driven by higher tax collections (+3.4%), though non-tax income dropped sharply (-67.8%). Government spending slipped 0.7% Year-on-Year to PHP437.3bn. Cumulatively, the deficit reached PHP869.2bn YTD, up from PHP697bn for the same period last year, but remains within the revised PHP1.56tril full-year target. There is limited fiscal option to pump prime the economy.

Vietnam’s VN-Index declined 1.22% on profit taking after strong performance in the previous two months (July: +8.84% and August: +11.3%). The World Bank trimmed its 2025 growth forecast for Vietnam to 6.6% from 6.8% and well below the government’s 8.3%-8.5% target, citing moderating activity as export growth normalizes after a strong first half. Vietnam’s exports to the United States, its largest export market fell 2% from the previous month to USD 13.94bn in August 2025, due to the imposition of new US tariffs, according to data released by Vietnamese Customs.

Market optimism over the election of Donald Trump as the new US President on expectations that his policies would be positive for the US had sparked a recalibration of macro variables and asset allocation decision. However, the US Administration’s subsequent tariff announcements and the inconsistent and frequent policy changes made in their wake had led to heightened market gyrations and volatility. Following the broad sell off after the announcement of across-the-board reciprocal tariffs on “Liberation Day”, the markets have recovered much of their losses as the shifting tariffs landscape seem to have reached some stability. With the finalization of tariff rates with majority of US’ trading partners, trade matters are heading into tailwind, at least for now. As for the US tariff for China, the US and China teams held the third round of bilateral meeting in Stockholm in late July. There was no announcement of any agreement, but both sides signaled willingness to continue negotiations. It remains a matter of conjecture as to whether the tariff dusts have really settled, as there appears to be a propensity for issues to burst to the surface that could change what has been agreed. Moreover, tied to the so called tariff agreements are commitments on investments and spendings to be made by the trading partner, and it is uncertain how these would pan out. In the light of the higher tariffs on imports into the US, economic forecast may have factored in slower global trade going forward, but actual impact remains to be seen.

During his Presidential election campaign, Donald Trump had also pitched to bring about a quick end to the Russia-Ukraine war should he be elected. Since his inauguration as US President, Trump has made moves, seeking to bring about a cessation of the conflict in Ukraine. The latest being a face-to-face Summit between him and President Putin held in Anchorage on August 15. An end to the Ukraine conflict would be positive for the equity markets. However, a peaceful resolution of the conflict does not appear to be any nearer. It remains to be seen if Trump and his Administration will succeed in orchestrating a cessation of the conflict in Ukraine. If this does come about, it would change the geo-political situation in Europe and elsewhere. Meanwhile, the Middle East remains a hot spot given the tense situation between Iran and Israeli, and Israel’s continuing military actions in Gaza. The geopolitical headwinds remain.

The US Fed decided to lower rates by 25 basis points in September. The market sees further reductions in the rest of the year and early 2026. The shift of market focus to dovish monetary stance will likely to be supportive of risk assets in near term. The market is still divided on impact of higher tariffs on macro variables such as inflation and economic activities. US corporate earnings especially in the technology sector continue to be key pillar to hold up risk assets. High valuation is further supported by strong capital expenditure drive for AI.

We are watchful of geo-political developments as well as policy directions in the major economies, in particular US and in China. The market is keenly watching developments in Trump’s tariffs for the key trade partners. The market is also attentive to other US policy pronouncements that would have major fiscal, financial and economic implications. Investors, by and large, appear to be comfortable with Trump’s “Big Beautiful Bill” that has been signed into law, notwithstanding that it will substantially increase US federal deficit and government debt. Meanwhile, failure by the US to pass a Bill to raise US’ debt ceiling has resulted in shutdown of the US government. However, US investors are not unduly concerned about this development, and the US market has taken it in its stride.

In Asia, the focus is on the pace of China’s economic recovery which has been weaker than expected. The tariff issues with the US can only exacerbate the economic situation in China. The Chinese property sector continues to face challenges, and any sign of stabilization and growth will have positive catalyst for China’s economy and risk assets. The Chinese government continues to bring forth various measures to help the economy. In September 2024, the Chinese government announced a slew of monetary, fiscal and policy measures to stimulate investment and consumption, enhance liquidity and restore confidence in the property and financial markets. Since then, there were additional measures taken. The Chinese government remains constructive on policies to spur economic activities to achieve economic growth target. The various measures have boosted market sentiments. However, the longer- term effectiveness on China’s economy continues to be closely watched. It may take time for the initiative to bear fruits. The focus will be on addressing the challenges in the property market, lifting consumer sentiments and consumption, and countering the effects of the new US tariffs.

On external trade, countries with high export dependency for growth in the Asia region including ASEAN will face significant challenges arising from the US tariff policies, even at the agreed rates that are significantly below the levels announced by the US during the “Liberation Day”. The disruption in supply chain realignment may result in temporary mismatch in corporate earnings delivery against market expectation during the initial stage of tariff implementation. This can result in further trading volatility for risk assets. Longer-term, higher tariffs may result in corporate margin erosion and slower earnings growth outlook. Consumers in the importing country may have to pay higher prices, and this translates to higher inflation rate.

While interest rates have started to be eased, there remains headwind for risk assets, including the impact of the still high interest rate on business and economic activities, uncertainties in the US policies post the US Presidential election, the still historically high market valuations in the US, the continuing geo-political tension in Europe, Middle East and in East Asia, and the still slower than expected economic growth in China. However, in the investment space we are in, we believe there is room for cautious optimism. After years of prolonged sell down, and despite the upticks in recent months, China equities are under-owned and their favourable valuation offer potential upside, particularly following the recent rounds of significant policy change initiatives from China. Also, the prospect of further softening of the US dollar could see increasing funds flow out of US assets which could be beneficial for emerging markets including China and ASEAN.

We are watchful of geo-political developments as well as policy directions in the major economies, in particular US and in China. The market is keenly watching developments in Trump’s tariffs for the key trade partners. The market is also attentive to other US policy pronouncements that would have major fiscal, financial and economic implications. Investors, by and large, appear to be comfortable with Trump’s “Big Beautiful Bill” that has been signed into law, notwithstanding that it will substantially increase US federal deficit and

We continue to apply our strategy of focusing on identifying fundamentally healthy companies with low valuations, low leverage, high growth, robust management and a strong track record, and adherence to our investment philosophy of “Never Fully Invest at All Times” which has served us well over the years. We thank you once again for your continued faith in us, and hope to remain good stewards in our endeavour to protect and grow your capital.